If you’re planning to live, work, study, invest, or apply for immigration in the United States, you’ve likely heard one warning on repeat:

“Don’t go uninsured in America.”

But how much is health insurance in America—really?

The frustrating answer: it depends on who you are, where you live, how you get coverage, and how much risk you’re willing (or able) to take.

This guide breaks it down clearly using the latest available data, real-world examples, and practical steps—so you can:

- Understand typical health insurance costs in the USA

- Compare employer, marketplace, private, and visitor options

- See what drives the price up (or down)

- Avoid nasty surprises like $30,000+ hospital bills

- Get your documents in order if you’re applying from overseas or in another language

And when your application or supporting documents aren’t in English, USCIS Official Translation is here to make sure language is never the reason your coverage or immigration process is delayed.

This guide is written with non-US citizens, new arrivals, and sponsors in mind, as well as US residents comparing their options.

Short Answer — How Much Is Health Insurance in America?

Here’s a high-level snapshot of what people are paying in 2025:

- Employer-sponsored health insurance (job-based):

- Average annual premium (single): around $9,300

- Average annual premium (family): around $27,000

- Workers typically pay only part of this (e.g. ±$1,400 for single, ±$6,800 for family), the rest is paid by employers.

- ACA Marketplace (Obamacare) individual plans (before subsidies):

- Benchmark (Silver) plan for a typical 40-year-old:

- ~$500/month in 2025 (up from $473 in 2024).

- Many enrollees pay far less after tax credits, with some eligible households paying close to $0–$100/month.

- Benchmark (Silver) plan for a typical 40-year-old:

- Employer vs Marketplace:

Average Marketplace premiums and employer premiums are now in a similar range per person, but employer plans often share costs more generously; Marketplace affordability heavily depends on income-based subsidies. - Go uninsured?

A three-day hospital stay can easily approach $30,000 before insurance. Serious emergencies or surgery can run into the tens or hundreds of thousands of dollars.

So, when people ask, “How much is health insurance in America per month?” a realistic range is:

- With job-based cover: roughly $120–$600+/month out of pocket for many employees (their share).

- Buying your own plan (before subsidies): roughly $350–$800+/month for a typical adult, depending on age, state, and plan level.

- Families: often $800–$2,500+/month in total premiums (employer + employee or fully self-paid).

The numbers above are premiums only. Your real annual cost depends on your deductible, copays, coinsurance, and out-of-pocket maximum. A cheap premium with a brutal deductible can cost you more than a slightly higher premium with better protection.

The rest of this guide explains why there’s so much variation—and how to choose smartly.

The 4 Main Ways People Get Health Insurance in the USA

1. Employer-Sponsored Health Insurance

Most under-65 Americans get health cover through their job.

For most full-time employees, this is the default option. Your employer selects the insurer and plan, pays a large share of the premium, and deducts your share from your salary.

Why it matters: usually the most cost-effective, simplest route if you’re eligible. Often better coverage, lower deductibles, and employer pays ±75–85% of the premium.

In 2025, the average annual premium for employer cover is about $9,325 for single and $26,993 for family coverage, with workers paying roughly $1,440 and $6,850 of that respectively.

Typical 2025 ballpark:

- Total premium for family coverage ≈ $27,000/year, with workers paying roughly a quarter and employers the rest.

- Single coverage ≈ high $8,000s–low $9,000s/year, with a smaller employee share.

Best for you if: you have access to a solid employer plan—it’s usually cheaper and more straightforward than buying alone.

2. ACA Marketplace (Healthcare.gov & State Marketplaces)

Designed for people who don’t get insurance through an employer (self-employed, part-time, freelancers, many immigrants, some students).

You shop on Healthcare.gov or a state marketplace, choose a plan, and may receive income-based subsidies that reduce your monthly premium.

For 2025, many states see benchmark Silver premiums for a 40-year-old in the rough $450–$550/month range before subsidies, with large variation by state. With tax credits, many eligible households pay well under $100/month.

If you don’t get insurance through work (self-employed, part-time, between jobs, some immigrants and students), you typically look at Affordable Care Act (ACA) Marketplace plans.

Plans are grouped into Bronze, Silver, Gold, Platinum:

- Bronze: Lowest premiums, highest deductibles.

- Silver: Middle ground; subsidies (tax credits & cost-sharing reductions) are usually linked to Silver.

- Gold/Platinum: Higher premiums, lower out-of-pocket costs.

Premium reality:

- Average benchmark Silver plan for a 40-year-old:

- About $500/month in 2025 (before subsidies), varying widely by state.

- Many households receive tax credits that sharply reduce this—sometimes to under $100/month.

Best for you if: you don’t have employer cover and your income qualifies for subsidies, or you want regulated, comprehensive coverage.

3. Public Programs (Medicaid & Medicare)

Medicaid is for eligible low-income individuals and families; Medicare primarily for people 65+ and some with disabilities.

These are government programmes, not typical private policies—if you qualify, they can drastically reduce your costs.

- Medicaid: For eligible low-income adults, children, pregnant people, elderly with low income, and some disabled individuals. Often low or no premium, with limited cost-sharing.

- Medicare: For most people 65+ or with certain disabilities.

Costs vary (Parts A, B, D, Medigap, Advantage), but this guide focuses on under-65 and private-style cover.

If you’re unsure of eligibility, always check official government sites rather than relying on third-party ads.

4. Short-Term, Expat & Visitor Insurance

These plans are aimed at visitors, international students, digital nomads, newly arrived workers, or anyone needing temporary cover while they are not yet eligible for comprehensive US insurance.

Premiums can look low, but cover is usually limited to emergencies, with exclusions for pre-existing conditions and ongoing treatment. They are a safety net for short stays, not a full solution if you’re settling long term.

If you’re:

- a visitor,

- an international student,

- on a temporary visa,

- or waiting for employer coverage to start,

you might use short-term or travel medical insurance.

These policies:

- Can be cheaper per month

- But often cover emergencies only and exclude pre-existing conditions.

They’re not substitutes for full U.S. health insurance if you’re settling long-term, but they’re better than no cover at all.

What Actually Drives the Price of Health Insurance in the US?

When you ask, “How much is health insurance in the US?”, these variables decide your number:

1. Age

Older applicants pay more—especially on individual plans. A 60-year-old can pay 2–3x more than a 25-year-old.

2. State & ZIP Code

Premiums vary sharply:

- High-cost states (e.g. New York, Alaska, Vermont) vs lower-cost states (e.g. Maryland, Indiana) see big differences driven by provider prices, regulation, and local competition.

3. Plan Metal Tier & Coverage Level

- Bronze: low premium, very high deductible → painful if you actually need care.

- Gold/Platinum: high premium, better if you expect regular treatment, prescriptions, or ongoing conditions.

4. Employer Contribution & Subsidies

- Generous employer = significantly lower personal cost.

- On the Marketplace, tax credits based on income can turn a $500 sticker price into an affordable monthly payment—or nothing at all for eligible households.

5. Health Status & Use of Care

While ACA plans cannot price you individually based on most medical conditions, your choice of plan should reflect your likely usage:

- Chronic conditions → richer coverage often cheaper long-term.

- Young, low-use → can tolerate higher deductible if you can afford worst-case scenarios.

6. Smoking & Lifestyle

In many states, smokers can legally be charged more.

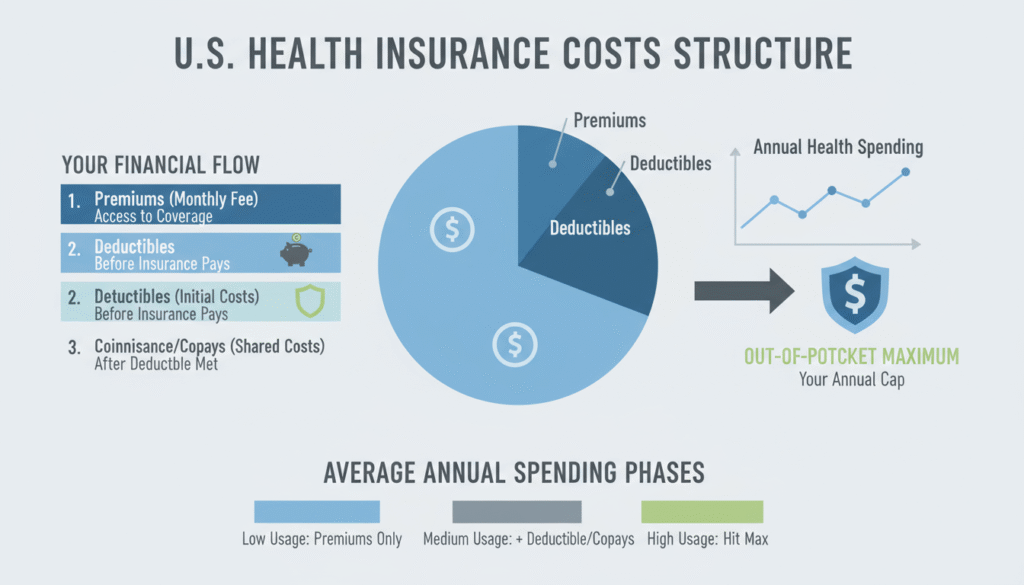

Premiums Are Only Half the Story — Your True Annual Cost

A common mistake: focusing only on “How much is health insurance in America per month?” and ignoring the rest.

You must also factor in:

Deductible

What you pay before your insurer starts sharing costs.

- Many popular plans have deductibles from $1,500 to $8,000+ per person.

- High-deductible plans pair with HSAs (tax-advantaged savings).

In many common 2025 plans, deductibles range from about $1,500–$8,000+ per person. Lower premiums usually mean higher deductibles.

Copayments & Coinsurance

After your deductible:

- Copay: fixed amount (e.g. $25 for a GP visit).

- Coinsurance: percentage (e.g. 20% of a hospital bill).

For example, after meeting your deductible, you might still pay 20% of a $10,000 bill ($2,000).

Out-of-Pocket Maximum (OOP Max)

The safety net: once your combined spending on deductibles, copays, and coinsurance hits this cap, the insurer pays 100% of covered costs for the rest of the year.

Regulated plans have set maximums each year; always check the latest figures on official government sources.

Marketplace and many employer plans have a regulated maximum each year; once you hit it, covered costs are paid at 100% for the rest of the year. Always check this number—it’s your worst-case scenario.

Example: Same Premium, Very Different Reality

Two people each pay $400/month ($4,800/year) for health insurance:

- Plan A

- Deductible: $7,500

- OOP Max: $9,000

- Good for: someone young with savings, using little care.

- Plan B

- Deductible: $1,000

- OOP Max: $3,500

- Good for: someone with ongoing treatment who’d hit the deductible anyway.

Lesson: The “cheapest” policy can be brutally expensive on the day you actually need it.

When comparing plans, always look at (1) annual premiums + (2) realistic usage + (3) worst-case up to the OOP max—not the monthly price in isolation.

Is Health Insurance in the USA “Worth It”?

Short answer: yes—if you can possibly afford it.

Without insurance, Americans and visitors face:

- $150–$300+ for a routine emergency room visit (before tests/treatment).

- Thousands for scans or minor surgery.

- Tens of thousands for hospital stays or serious illness.

A single uninsured medical event can derail a visa plan, career, or business—and in some immigration cases, unpaid hospital debt can complicate future applications.

Being properly insured is financial protection, not a luxury.

How to Choose the Right Health Insurance (Residents, Expats & Newcomers)

Step 1 — Define Your Situation

Ask yourself:

- Are you employed in the US with benefits?

- Self-employed or contractor?

- International student?

- New immigrant or on a work/family/entrepreneur visa?

- Bringing dependants?

Your category decides whether your best path is employer plan, ACA Marketplace, Medicaid, Medicare, or private/visitor cover.

If you’re on a visa or recent immigrant, your route is usually:

- employer plan if your US employer offers one,

- ACA Marketplace if you meet immigration and residency rules,

- or reputable expat/visitor cover for shorter stays or while you’re waiting to qualify.

Step 2 — Map Out Your Annual Budget

Include:

- Premiums (12 months)

- Likely routine costs (GP visits, prescriptions, therapy, tests)

- Worst-case scenario (hit the OOP max)

If that “pain number” would bankrupt you, increase your coverage level.

Step 3 — Check Network & Hospitals

Always confirm:

- Are your preferred doctors/hospitals “in-network”?

- Does the plan work in the state(s) you’ll actually live in or travel to?

Out-of-network surprises are a classic (and expensive) trap.

Step 4 — For Non-US Documents: Fix the Language Gap Early

If your insurer, employer, university, or the Marketplace requires:

- Birth certificates

- Marriage certificates

- Medical records

- Vaccination records

- Proof of income or employment

- Immigration notices or USCIS documents

…and they’re not in English, they may ask for a certified translation.

This is where USCIS Official Translation supports you:

- Certified translations accepted by U.S. authorities, insurers, universities, and legal bodies

- Fast turnaround for time-sensitive enrollments

- Clear formatting that mirrors your original documents

USCIS Official Translation provides certified translations that match insurer and USCIS expectations, so your enrolment or application is not delayed because of documentation issues.

Upload your documents now to get a certified translation quote for your health insurance or immigration paperwork — no obligation, fast response.

Why Is American Health Insurance So Expensive?

Several structural reasons:

- High hospital and specialist fees

- Expensive prescription drugs (especially new therapies)

- Administrative complexity (multiple payers, billing systems)

- Cost of new technology and procedures

- Limited price regulation in many markets

For many, premiums have grown faster than wages—especially in recent years—putting pressure on both employers and families.

Understanding this context helps explain why “cheap but inadequate” plans are so risky: the underlying care is costly.

Practical Scenarios — How Much Might You Pay?

These simplified examples combine premiums + likely usage + potential worst-case costs, so readers can see how the numbers play out in real life.

Example 1 — Young Professional in New York (Single)

- Age: 29

- Income: $70,000

- No employer cover, buys ACA plan

- Likely range: $350–$550/month before any tax credits, depending on plan level; limited or no subsidy at this income.

Example 2 — Family of Four in Texas with Employer Plan

- Employer-sponsored PPO

- Total premium: roughly $24,000–$27,000/year

- Employee share: maybe $5,000–$7,000/year (about $420–$580/month), plus deductibles and copays.

Example 3 — Newcomer on a Work Visa

- Employer offers basic plan with 70–80% paid by employer

- Employee cost: perhaps $150–$300/month for single coverage

- Needs certified translation of foreign health records & civil documents for HR and insurers.

Contact us today to translate your supporting documents accurately before you submit your application or enrollment forms.

Do You Need Certified Translation for Health Insurance or USCIS-Related Processes?

You may be asked for certified translations when:

- Applying for health insurance as a new arrival and proving identity, dependants, or prior coverage

- Enrolling children in coverage with foreign birth or adoption documents

- Submitting medical reports or vaccination records from another country

- Handling USCIS cases (green card, adjustment of status, waivers) where financial responsibility and insurance are reviewed

- Providing documents to universities, employers, or sponsors

USCIS Official Translation provides:

- Certified, accurate translations from 100+ languages into English

- Formatting aligned with insurer and USCIS expectations

- Statement of accuracy, translator details, and seal where required

- Fast, secure digital delivery

“Need certified translations for your U.S. health insurance or immigration file? Get a Quote.”

Data Sources Used in This Guide

This guide is based on the latest available data at the time of writing, including:

- KFF 2025 Employer Health Benefits Survey – average premiums for single and family employer-sponsored coverage.

- KFF 2024 Employer Health Benefits Survey – 2024 benchmarks used for year-on-year comparisons.

- Centers for Medicare & Medicaid Services (CMS) – 2025 Qualified Health Plan (QHP) Marketplace premium and choice data.

- Urban Institute & other independent analyses of 2025 Marketplace premiums and age-rating patterns.

- Additional reputable sources cited throughout where specific figures are referenced.

All figures are rounded and meant as realistic ranges, not personalised quotes. Always check current premiums on official government or insurer websites before making decisions.

FAQs — How Much Is Health Insurance in the US?

How much is health insurance in America per month on average?

For many adults buying their own plan, expect roughly $350–$800+ per month before subsidies, depending on age, state, and coverage. With subsidies, some eligible applicants pay under $100/month. Employer plans often reduce your share significantly.

How much does health insurance cost in the US for a family?

A typical employer-sponsored family plan now costs around $27,000/year in total premiums, with employees paying roughly $6,000–$7,000 on average and employers covering the rest. Marketplace family premiums vary widely but are heavily influenced by subsidies.

Why is American health insurance so expensive?

Because medical care, prescription drugs, and hospital services are expensive, pricing is fragmented, and there is limited central regulation of prices. Administrative complexity and new high-cost treatments also drive premiums higher.

Is it ever okay to go without health insurance in the USA?

It is extremely risky. A single emergency can cost more than years of premiums. If standard plans feel unaffordable, explore Medicaid (if eligible), subsidised ACA plans, or short-term/visitor plans rather than going fully uninsured.

I’m moving to the US. Do I need certified translations for my health insurance?

Often yes. Insurers, employers, universities, and immigration authorities may require key documents (birth certificates, marriage certificates, medical reports) in English. Certified translations help ensure your application is processed smoothly and taken seriously.

Which health insurance providers operate in the USA?

Major providers include companies like UnitedHealthcare, Kaiser Permanente, Blue Cross Blue Shield affiliates, Aetna, Cigna, and others. Availability depends on your state and plan type. Always compare networks, coverage, and total yearly costs—not just premiums.